What is the Difference Between Chapter 7 and 13 Bankruptcy?

Chapter 7 Vs Chapter 13 Bankruptcy

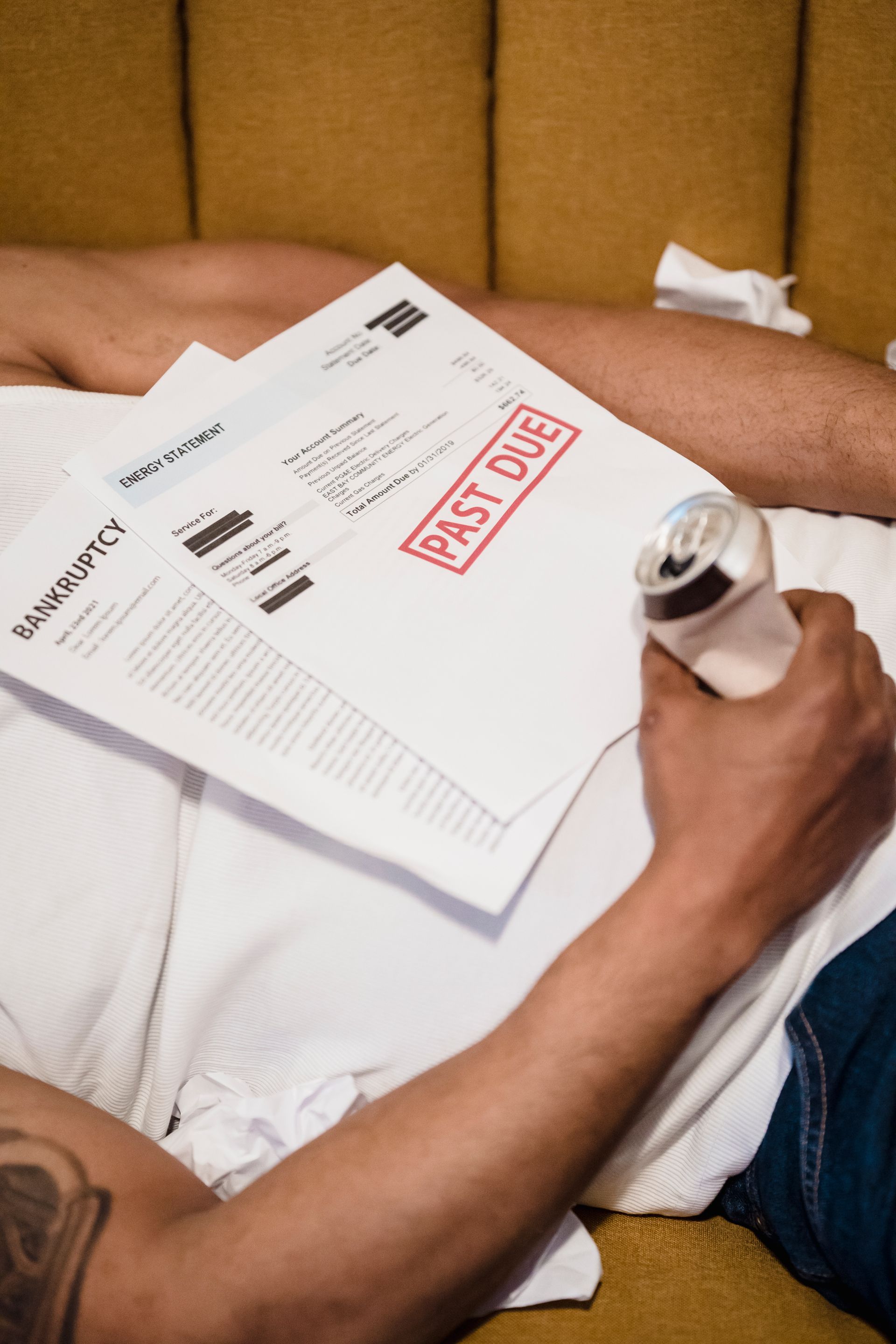

Bankruptcy is not a straightforward process. There are several options when it comes to debt relief. You can enter a repayment plan or file bankruptcy. There are two key types of bankruptcy: chapter 7 and chapter 13. Both clear unsecured debt such as credit card debt and medical payments. The right choice for your situation depends on many factors. Here are some of the key differences between chapter 7 and 13 bankruptcy:

Chapter 7

Chapter 7 bankruptcy dissolves your unsecured debt without any need for repayment. You must pass the chapter 7 means test. It will take up to several months to see your debt relieved. Individuals and business entities are both eligible for chapter 7.

Chapter 13

Chapter 13 is the reorganization of your debt. You will enter a court-mandated repayment plan. Upon completion of your repayment plan, your unsecured debt will be forgiven. Secured debt may be forgiven if the collateral is given up by the debtor. For example, giving up your vehicle to the holder of your auto loan may relieve your auto loan. Only individuals and sole proprietors are eligible for chapter 13 bankruptcy.

Contact Our Bankruptcy Attorney Today!

At the Law Office of Wendy J. Christophersen, we assist clients with filing for chapter 13 and chapter 7 bankruptcy. The right type of bankruptcy for you depends on several factors including the amount of debt, the types of debt you have, and your ability to repay it. Our lawyers will help you decide which options you are eligible for, and which is best for you. Contact us today to schedule your initial consultation!